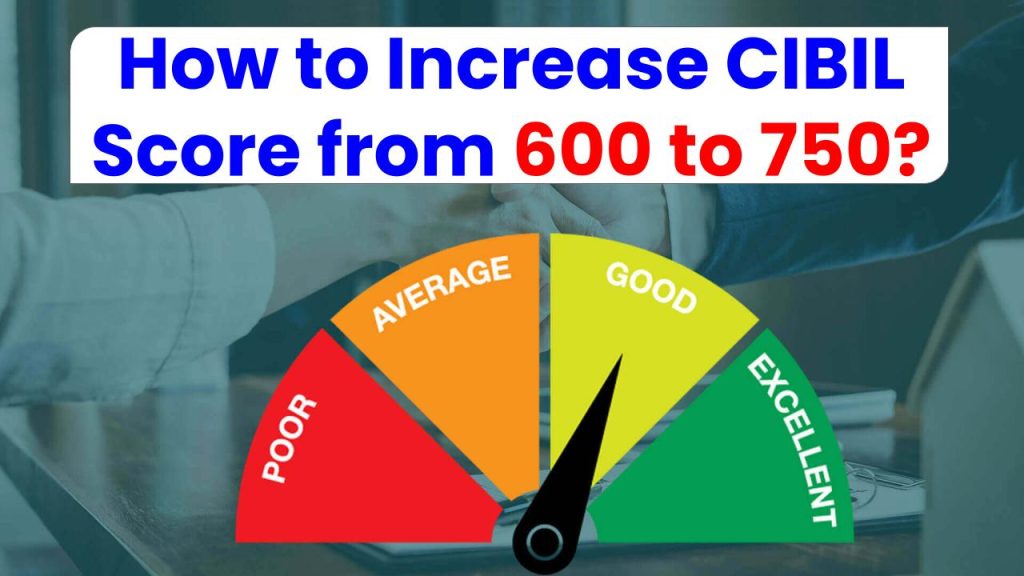

If you’re wondering how to increase CIBIL score from 600 to 750, you’re not alone! Many people struggle to get approved for loans or credit cards because of a low CIBIL score. But here’s the good news—improving your credit score is absolutely possible with a little discipline, strategy, and knowledge.

Whether you’re planning to buy a house, apply for a personal loan, or even get a credit card, having a CIBIL score above 750 can unlock the best interest rates and offers. Let’s break down the easiest, most effective steps to help you boost your score—and secure that loan you need!

Increase CIBIL Score from 600 to 750

| Key Details | Insights |

|---|---|

| Ideal CIBIL Score for Loan Approval | 750+ |

| Current Low Score Example | 600 |

| Main Factors Impacting Score | Payment history, credit utilization ratio, credit mix, loan applications, credit report errors |

| Average Time to Improve Score | 6 months to 1 year (with disciplined credit behavior) |

Improving your CIBIL score from 600 to 750 is not as hard as it seems—it simply requires consistency, financial discipline, and awareness. By following the five steps outlined above, you can boost your score, improve your loan eligibility, and access better credit deals.

What is a CIBIL Score and Why is it Important?

A CIBIL score is a three-digit number (ranging from 300 to 900) that represents your creditworthiness. Banks, NBFCs, and financial institutions use this score to determine if you’re a reliable borrower. The higher the score, the better your chances of getting loans approved at favorable interest rates.

A score of 750 and above is typically considered excellent. A score around 600 or below signals risk to lenders, making it harder to secure loans or credit cards.

see also: Post Office or Bank, Where to Do Tax-saving FD?

5 Easiest Steps to Increase Your CIBIL Score from 600 to 750

1. Make Timely Payments – Every Single Time!

Payment history accounts for nearly 35% of your score. Missing EMI or credit card payments is one of the biggest reasons for a low score.

How to do this:

- Set up auto-debit for EMIs and credit card bills.

- Mark calendar reminders days before due dates.

- Pay at least the minimum due amount if unable to pay in full.

Example: If you have a personal loan EMI of Rs. 10,000, ensure it’s paid before the due date every month without fail. Even one missed payment can dent your score.

2. Keep Credit Utilization Below 30%

Credit utilization ratio is the percentage of credit limit you use. Using too much of your available limit shows lenders you may be over-dependent on credit.

How to manage:

- Spend less than 30% of your total credit limit.

- Request a credit limit increase (but avoid increasing spending).

Example: If your credit card limit is Rs. 1 lakh, try not to spend more than Rs. 30,000 monthly.

3. Avoid Multiple Loan/Credit Card Applications in a Short Span

Each time you apply for a loan, the lender checks your credit report (known as a hard inquiry). Too many applications in a short time can reduce your score and make you look credit-hungry.

What you should do:

- Apply for loans only when necessary.

- Research lenders’ eligibility criteria before applying to avoid rejection.

Example: Instead of applying for three personal loans from different banks at once, check where you meet the eligibility criteria and apply only to one.

4. Diversify Your Credit Mix

Lenders like to see a healthy mix of secured loans (home loans, auto loans) and unsecured loans (credit cards, personal loans).

Action steps:

- Don’t rely solely on credit cards.

- Consider responsibly taking a small secured loan and repaying it promptly.

Example: Having a home loan and one credit card, both paid on time, is better for your credit score than just having multiple unsecured loans.

5. Regularly Monitor and Correct Your Credit Report

Sometimes, errors on your credit report (like incorrect account details or wrong outstanding amounts) can pull your score down unnecessarily.

Steps to follow:

- Check your credit report every 3-6 months.

- Dispute incorrect information directly with CIBIL via their website.

Example: You might find an old loan marked as unpaid even after settlement. Rectifying this can improve your score significantly.

How Long Does It Take to Improve Your CIBIL Score?

Typically, with disciplined credit behavior, you can improve your score from 600 to 750 in 6 months to 1 year. It depends on factors like payment consistency, current debts, and utilization rates.

Why Is a High CIBIL Score Essential for Loans and Credit Cards?

| Score Range | Loan Approval Chances | Interest Rate Benefits |

|---|---|---|

| 750+ | High | Low-interest rates, best offers |

| 650 – 749 | Medium (may require extra checks) | Standard rates |

| Below 650 | Low | High-interest rates, loan rejections possible |

Financial institutions prefer borrowers with higher scores, as they are considered low-risk.

see also: How Many Times a Year and On Which Date of the Month Do You Get Savings Interest?

Increase CIBIL Score from 600 to 750 FAQs

1. Can I increase my CIBIL score in one month?

Raising your score significantly in one month is challenging. However, small improvements are possible by reducing credit utilization and ensuring all payments are timely.

2. Will closing old credit cards improve my CIBIL score?

Not necessarily. Closing old cards reduces your credit history length, which may negatively impact your score. It’s better to keep them active and use them occasionally.

3. How often should I check my credit report?

It’s advisable to check your credit report every 3 to 6 months. You can get a free report annually from the CIBIL website.

4. Is credit repair legal in India?

Yes, but be wary of companies promising “instant fixes.” Follow legitimate steps like making timely payments and correcting errors via official channels.