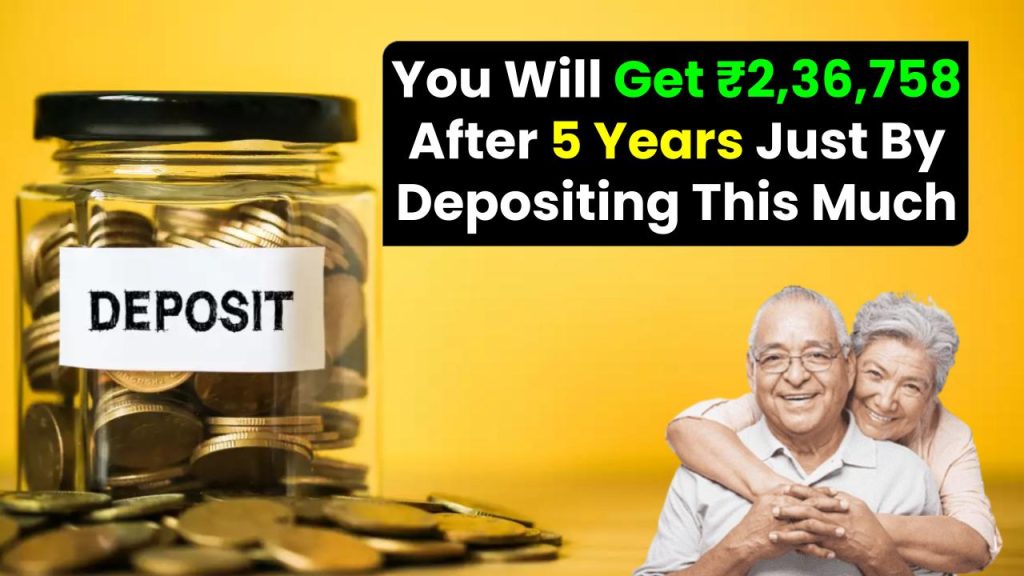

The NSC Scheme, or National Savings Certificate, is a popular small savings investment plan backed by the Government of India. If you’re looking for a safe, low-risk option with guaranteed returns, NSC is worth considering. In fact, you can get ₹2,36,758 after 5 years by making a smart one-time deposit today. But how much should you invest to reach that amount?

Let’s break it down in this easy, step-by-step guide that shows exactly how the NSC works, how much to deposit, the interest it earns, and why this scheme remains one of the most trusted savings instruments in India.

NSC Scheme

| Feature | Details |

|---|---|

| Scheme Name | National Savings Certificate (NSC) |

| Interest Rate | 7.7% p.a. (compounded annually, paid at maturity) |

| Tenure | 5 Years |

| Minimum Investment | ₹100 (in multiples of ₹100) |

| Maximum Investment | No upper limit |

| Investment for ₹2,36,758 Return | ₹1,63,200 (one-time deposit) |

| Tax Benefits | Deduction under Section 80C of Income Tax Act (up to ₹1.5 lakh) |

| Official Website | India Post |

If you’re looking for a secure, tax-saving investment with fixed returns, the NSC is an excellent choice in 2025. With the 7.7% annual return, it offers better post-tax yield than many bank FDs, especially for those in the lower or moderate tax brackets.

An investment of just ₹1.63 lakh today could grow to ₹2.36 lakh in 5 years without you having to worry about market risks. Whether you’re a working professional, a parent, or a retiree, NSC offers a simple, low-maintenance route to grow your savings.

What Is NSC and Why Is It So Popular?

The National Savings Certificate (NSC) is a fixed-income investment scheme available at all post offices in India. It is designed to encourage small to mid-level savings for salaried individuals, small business owners, senior citizens, and conservative investors who prefer guaranteed returns over market-linked risks.

Key Benefits:

- Guaranteed returns: Your money grows at a fixed interest rate.

- Backed by the Government of India: Safe and secure.

- Tax saving: Enjoy deductions under Section 80C up to ₹1.5 lakh.

- Compounding advantage: Interest is compounded annually and paid out at maturity.

see also: Invest ₹5,000 Every Month and Create ₹6 Crore Wealth for Your Child

How Much Should You Deposit to Get ₹2,36,758 After 5 Years?

Let’s get straight to the numbers. The current interest rate for NSC is 7.7% per annum (as of Q1 FY 2024-25), compounded annually. Using the compound interest formula:

Maturity Amount (M) = P × (1 + r/100)^n

Where:

- M = Maturity amount = ₹2,36,758

- r = Interest rate = 7.7%

- n = Tenure = 5 years

Rearranging the formula to calculate the investment (P):

P = M / (1 + r/100)^n P = 2,36,758 / (1.077)^5 = ₹1,63,200 approx

So, by investing just ₹1,63,200 today in NSC, you will get ₹2,36,758 after 5 years.

Who Should Consider Investing in NSC?

The NSC scheme is ideal for:

Salaried Individuals:

Looking for a safe investment option that also helps with tax saving under 80C.

Senior Citizens:

Who want fixed income options without market risks.

First-Time Investors:

Looking for simple and secure investments.

Parents Planning for Education:

Start with Just ₹1000 and Get Huge Profits in 5 Years: Post Office FD Scheme New Interest Rates 2025

Use NSC to build a fixed corpus over 5 years for child education expenses.

Step-by-Step Guide to Invest in NSC

Step 1: Visit Your Nearest Post Office

You can open an NSC account at any India Post Office branch.

Step 2: Fill the NSC Application Form

You need to submit:

- Passport-size photo

- PAN card

- Aadhaar (mandatory for KYC)

- Address proof (utility bill, passport, etc.)

Step 3: Make the Deposit

Minimum deposit is ₹100. You can invest any amount in multiples of ₹100.

Step 4: Collect the Certificate or Account Details

Earlier, NSC was issued as a physical certificate. Now, investments are done in electronic mode linked to your Post Office Savings Account.

Tax Benefits of NSC

- Deduction under Section 80C: You can claim up to ₹1.5 lakh in a financial year.

- Interest earned every year is taxable, but it is deemed reinvested, so it qualifies again for 80C (except interest earned in the final year).

see also: This is How a Fund of Rs 12 Thousand to Rs 1 Crore Will Be Created

NSC vs Other Popular Savings Schemes

| Feature | NSC | PPF | FD (Bank) |

|---|---|---|---|

| Tenure | 5 years | 15 years | 1-10 years |

| Interest Rate | 7.7% | 7.1% (Q1 FY25) | 6.5% – 7.5% (varies) |

| Tax Saving | Yes (80C) | Yes (80C) | Only under Tax Saver FD |

| Premature Withdrawal | Not Allowed | Allowed (conditions) | Allowed (with penalty) |

| Safety | Very High | Very High | Depends on bank rating |

NSC Scheme FAQs

1. Is NSC interest rate fixed?

Yes, once you invest, the rate remains fixed for the 5-year duration.

2. Can NRIs invest in NSC?

No, only resident Indians are eligible to invest in NSC.

3. What happens after 5 years?

The full maturity amount, including principal and interest, is paid to you. You can choose to reinvest if needed.

4. Can I withdraw NSC before maturity?

No. Premature withdrawal is not allowed except in case of death of holder or court orders.

5. Where can I check the current NSC rate?

You can visit the India Post Interest Rates Page for the latest updates.